COBRA Extensions 2026: Critical Deadlines for Continued Health Coverage

Understanding health insurance options, especially during periods of transition, is paramount. The Consolidated Omnibus Budget Reconciliation Act (COBRA) provides a vital safety net, allowing individuals and their families to maintain group health coverage after certain qualifying events. However, navigating the intricacies of COBRA, particularly with potential extensions and evolving regulations, can be complex. As we look towards 2026, it’s crucial to be aware of the latest COBRA extensions and the critical deadlines that could impact your continued coverage. This comprehensive guide aims to demystify these aspects, providing you with the knowledge needed to make informed decisions about your healthcare.

The landscape of healthcare legislation is ever-changing, and staying updated on provisions like COBRA is not just good practice—it’s essential for safeguarding your health and financial well-being. This article will delve into the specifics of COBRA, discuss any anticipated extensions for 2026, outline the key deadlines you need to mark on your calendar, and offer practical advice on how to ensure uninterrupted health coverage. Whether you’re facing a job change, a reduction in hours, or another qualifying event, understanding your COBRA rights and responsibilities for 2026 will be invaluable.

What is COBRA and Why is it Important for 2026?

COBRA is a federal law that gives workers and their families who lose their health benefits the right to choose to continue group health benefits provided by their group health plan for limited periods of time under certain circumstances such as voluntary or involuntary job loss, reduction in the hours worked, transition between jobs, death, divorce, and other life events. This continued coverage, however, is not free. Individuals typically pay the full cost of the premium, plus an administrative fee, which can be significantly higher than what they were paying as an active employee.

For 2026, the fundamental principles of COBRA remain the same, but understanding potential legislative adjustments or administrative interpretations is key. While no major, sweeping COBRA extensions akin to those seen during the COVID-19 pandemic are currently projected, it’s vital to monitor for any new developments. The importance of COBRA for 2026 cannot be overstated, as it serves as a critical bridge between employer-sponsored health plans and other coverage options, preventing gaps in healthcare access during vulnerable times.

Without COBRA, many individuals would find themselves without health insurance during periods of unemployment or other life changes, leading to potential financial ruin in the event of an unexpected illness or injury. Therefore, grasping the nuances of COBRA, especially concerning any COBRA extensions 2026, is a fundamental aspect of personal financial and health planning.

Key Qualifying Events That Trigger COBRA Rights

COBRA eligibility is not universal; it’s triggered by specific ‘qualifying events.’ These events dictate when an individual or their dependents can elect to continue their health coverage. Understanding these events is the first step in determining your eligibility for COBRA, and by extension, any COBRA extensions 2026. The primary qualifying events include:

- Termination of Employment (Voluntary or Involuntary): This is perhaps the most common trigger. If your employment is terminated for reasons other than gross misconduct, you and your dependents are typically eligible for COBRA. This includes layoffs, resignations, and firings, provided it’s not for gross misconduct.

- Reduction in Hours: If your work hours are reduced to a point where you no longer meet the employer’s eligibility requirements for group health plan coverage, this also qualifies.

- Death of the Employee: If an employee dies, their surviving spouse and dependent children can elect COBRA coverage.

- Divorce or Legal Separation: If an employee divorces or legally separates from their spouse, the ex-spouse and dependent children may elect COBRA.

- Employee Becomes Entitled to Medicare: If an employee becomes entitled to Medicare, their spouse and dependent children may still elect COBRA if they would otherwise lose coverage under the plan.

- Loss of Dependent Child Status: When a dependent child reaches an age where they are no longer considered a dependent under the plan’s rules (e.g., turning 26), they can elect COBRA coverage.

Each of these events initiates a specific timeline for notification and election, which we will explore in detail when discussing COBRA extensions 2026 deadlines. It’s crucial to remember that the employer must be notified of certain qualifying events (like divorce or a child losing dependent status) by the employee or qualified beneficiary within a specified timeframe for COBRA rights to be preserved.

Understanding the Standard COBRA Election and Coverage Periods

Before diving into potential COBRA extensions 2026, it’s essential to grasp the standard COBRA election and coverage periods. These timelines are strictly enforced, and missing a deadline can result in the forfeiture of your COBRA rights.

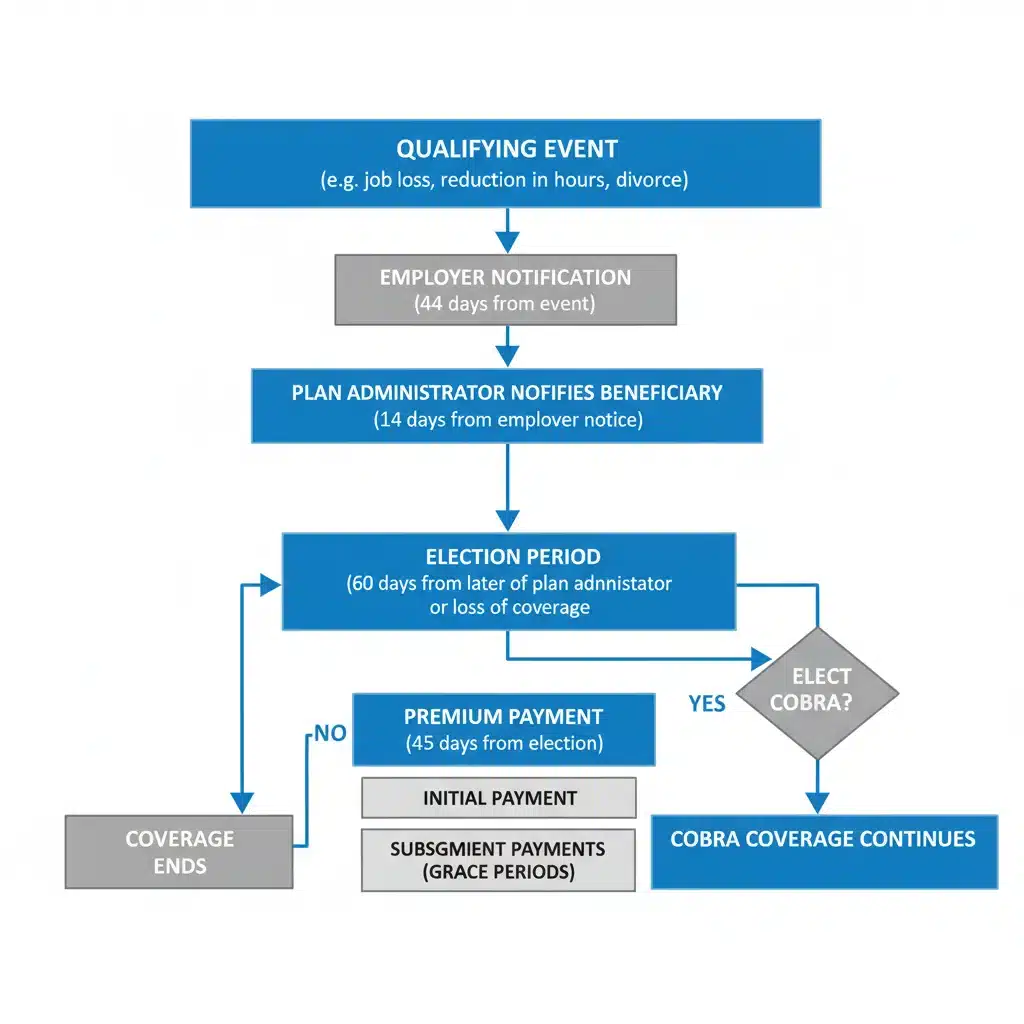

Employer Notification Period

Once a qualifying event occurs, the employer has a specific timeframe to notify the plan administrator. For most qualifying events (like termination or reduction in hours), the employer must notify the plan administrator within 30 days of the event. For events like divorce or a child aging out, the employee or qualified beneficiary must notify the plan administrator within 60 days of the event.

Plan Administrator Notification Period

After receiving notification from the employer or beneficiary, the plan administrator has 14 days to notify the qualified beneficiaries of their COBRA rights. This notice will include information about the plan, the coverage options, and the cost.

COBRA Election Period

Once a qualified beneficiary receives the election notice, they have 60 days to decide whether to elect COBRA coverage. This 60-day period begins on the later of the date the election notice is provided or the date group health coverage would be lost due to the qualifying event.

COBRA Coverage Duration

The standard duration of COBRA coverage varies depending on the qualifying event:

- 18 Months: For qualifying events such as termination of employment or reduction of hours.

- 36 Months: For qualifying events such as death of the employee, divorce or legal separation, or a dependent child losing eligibility.

These are the baseline periods. Any COBRA extensions 2026 would build upon or modify these standard durations.

Anticipated COBRA Extensions 2026: What to Expect

While the COBRA law itself is well-established, its application can be influenced by legislative changes, economic conditions, and public health emergencies. The most significant COBRA extensions in recent memory occurred during the COVID-19 pandemic, which provided extended deadlines for COBRA elections and premium payments. As of now, there are no specific federal legislative proposals for COBRA extensions 2026 that would replicate the broad relief seen during the pandemic. However, it is always prudent to remain vigilant for any potential developments.

It’s important to differentiate between general COBRA extensions and specific state-level ‘mini-COBRA’ laws, which may offer additional protections or longer coverage periods for smaller employers not subject to federal COBRA. These state laws vary widely and could provide additional avenues for continued coverage in 2026, even if federal COBRA remains unchanged.

Moreover, the Department of Labor (DOL) and other regulatory bodies occasionally issue guidance or clarifications that can impact COBRA administration. Staying informed about these pronouncements is crucial. While a large-scale federal extension similar to the pandemic relief might not be on the horizon, it’s not impossible for targeted relief or adjustments to be introduced, especially in response to unforeseen economic shifts or public health concerns. Therefore, individuals should monitor official government sources for any updates regarding COBRA extensions 2026.

Extended Coverage Due to Disability

One existing COBRA extension that is often overlooked relates to disability. If a qualified beneficiary is determined by the Social Security Administration (SSA) to be disabled within the first 60 days of COBRA coverage, they may be eligible for an additional 11 months of coverage, extending the standard 18-month period to 29 months. This extension is available to all qualified beneficiaries under the same qualifying event, not just the disabled individual. This provision is a permanent part of COBRA law and will continue to be relevant for COBRA extensions 2026.

To qualify for this extension, the plan administrator must be notified of the SSA’s disability determination within 60 days of the determination and before the end of the initial 18-month COBRA period. This highlights the importance of timely notification and understanding all potential avenues for extending coverage.

Second Qualifying Events

Another existing mechanism for COBRA extensions is a ‘second qualifying event.’ If a second qualifying event occurs during the initial 18-month COBRA coverage period (e.g., divorce or death of the former employee while the ex-spouse is on COBRA), the coverage for the qualified beneficiaries can be extended from 18 months to a maximum of 36 months from the date of the original qualifying event. This is an important consideration for those initially on 18-month COBRA coverage and should be kept in mind for COBRA extensions 2026 planning.

5 Critical COBRA Deadlines for 2026

Navigating COBRA requires a keen eye on deadlines. While the exact dates will depend on your specific qualifying event, here are 5 critical types of deadlines to be acutely aware of for COBRA extensions 2026:

1. Employer Notification of Qualifying Event (30 Days)

For qualifying events such as termination of employment or reduction in hours, your former employer has 30 days from the date of the event to notify the plan administrator. This notification kicks off the COBRA process. Failure of the employer to meet this deadline can have implications, but as a beneficiary, it’s primarily their responsibility. However, understanding this timeline helps you anticipate when you should receive your election notice.

2. Beneficiary Notification of Certain Qualifying Events (60 Days)

For other qualifying events, such as divorce, legal separation, or a child losing dependent status, the qualified beneficiary (you, your spouse, or your child) is responsible for notifying the plan administrator. This notification must occur within 60 days of the qualifying event. Missing this 60-day window can result in the loss of COBRA rights for that specific event. This is a critical self-managed deadline for COBRA extensions 2026 eligibility.

3. COBRA Election Period (60 Days)

Once you receive your COBRA election notice from the plan administrator, you have a strict 60-day period to elect COBRA coverage. This 60-day period starts from the date the notice was provided OR the date your group health coverage would have ended, whichever is later. It’s imperative not to miss this deadline. Even if you are unsure about electing COBRA, it’s wise to consider all options within this window. This is arguably the most crucial deadline for securing your COBRA extensions 2026.

4. Initial COBRA Premium Payment Due Date (45 Days After Election)

After you elect COBRA coverage, you have an initial grace period of 45 days to make your first premium payment. This 45-day period begins from the date you make your COBRA election, NOT from the date you receive the election notice or the qualifying event. It’s important to note that this first payment covers the entire period from the loss of coverage up to the date of the first payment. For subsequent premium payments, you generally have a 30-day grace period.

5. Notification of Disability or Second Qualifying Event for Extensions (60 Days)

If you are seeking COBRA extensions 2026 due to disability or a second qualifying event, timely notification is key. For disability, the plan administrator must be notified within 60 days of the Social Security Administration’s determination of disability and before the end of the initial 18-month COBRA period. For a second qualifying event (e.g., divorce after initial termination), the plan administrator must be notified within 60 days of that second event occurring. Missing these deadlines can jeopardize your ability to extend coverage beyond the initial 18 months.

How to Ensure Uninterrupted Coverage with COBRA Extensions 2026

Ensuring a smooth transition and uninterrupted health coverage requires proactive steps. Here’s how you can navigate COBRA effectively for 2026:

- Understand Your Rights: Familiarize yourself with the specifics of COBRA law, including qualifying events and standard coverage periods. Don’t assume anything; verify information directly with your former employer’s HR department or the plan administrator.

- Keep Records: Maintain meticulous records of all communications related to your employment termination or other qualifying event, as well as all COBRA notices received and sent. Date stamps, certified mail receipts, and email confirmations can be invaluable.

- Timely Notifications: Be acutely aware of the deadlines for notifying the plan administrator about qualifying events that are your responsibility (divorce, child aging out). Set reminders well in advance.

- Review Election Notices Carefully: When you receive your COBRA election notice, read it thoroughly. It will contain critical information about your coverage options, costs, and payment instructions. If anything is unclear, ask for clarification immediately.

- Budget for Premiums: COBRA premiums can be expensive, often including the full employer and employee contributions plus an administrative fee. Factor this into your financial planning. Explore alternative, potentially more affordable, coverage options on the Health Insurance Marketplace (healthcare.gov) during the special enrollment period that typically coincides with a loss of employer-sponsored coverage.

- Consider Alternatives: While COBRA is a valuable option, it’s not always the most cost-effective. Explore state marketplaces, Medicaid, or your spouse’s employer-sponsored plan. Compare benefits and costs carefully before making a decision.

- Seek Professional Advice: If your situation is complex, or you have questions about COBRA extensions 2026, consider consulting with a benefits specialist, financial advisor, or legal expert specializing in health law.

- Monitor for Legislative Changes: Stay informed about any potential federal or state legislative changes that could impact COBRA or introduce new COBRA extensions 2026. Official government websites (DOL, IRS) are reliable sources.

COBRA vs. Health Insurance Marketplace: Making the Right Choice for 2026

When facing a qualifying event, COBRA is often presented as the immediate solution for continued health coverage. However, it’s crucial to understand that it’s not the only option, and for many, it might not be the most affordable or suitable one. The Health Insurance Marketplace (established under the Affordable Care Act, or ACA) provides a significant alternative, especially when considering COBRA extensions 2026.

Cost Comparison

The primary difference often lies in cost. COBRA typically requires you to pay the full premium, including the portion your former employer used to cover, plus an administrative fee (up to 2% of the premium). This can make COBRA coverage quite expensive. In contrast, plans on the Health Insurance Marketplace may offer subsidies (premium tax credits and cost-sharing reductions) based on your income, making them significantly more affordable for many individuals and families. The loss of employer-sponsored coverage triggers a Special Enrollment Period (SEP) on the Marketplace, allowing you to enroll outside of the annual open enrollment period.

Coverage Options

COBRA allows you to continue the exact same health plan you had with your employer. This can be beneficial if you are happy with your current doctors and network. The Marketplace, however, offers a wider array of plans from different insurance companies, with varying levels of coverage (Bronze, Silver, Gold, Platinum) and provider networks. This can provide greater flexibility to choose a plan that best fits your specific health needs and budget for 2026.

Decision Factors for COBRA Extensions 2026

- Cost: If you qualify for significant subsidies on the Marketplace, it will likely be more affordable than COBRA.

- Doctor/Network Loyalty: If staying with your current doctors is a top priority and they are only in your former employer’s plan, COBRA might be worth the higher cost.

- Immediate Need: COBRA can offer immediate, seamless continuation of your existing plan. The Marketplace enrollment process might take a little longer to finalize.

- Anticipated Future Coverage: If you expect to secure new employer-sponsored coverage relatively quickly, COBRA might serve as a short-term bridge. If you anticipate a longer period without employer coverage, exploring Marketplace options for COBRA extensions 2026 might be more strategic.

It is highly recommended to compare the costs and benefits of both COBRA and Marketplace plans during your 60-day COBRA election period. Use the tools available on healthcare.gov to estimate subsidies and plan costs before making a final decision.

Common Misconceptions About COBRA and 2026 Extensions

Several myths surround COBRA that can lead to confusion and missed opportunities. Dispelling these misconceptions is vital for anyone considering COBRA extensions 2026.

- Myth: COBRA is Free. This is perhaps the most common misconception. COBRA is rarely free. You are typically responsible for 100% of the premium, plus an administrative fee. The only times it might be ‘free’ is if your former employer voluntarily subsidizes it, which is rare and usually for a very limited time.

- Myth: You Must Take COBRA. While COBRA is a valuable option, it’s not mandatory. You have the right to elect it, but you are also free to pursue other health insurance options, such as the Health Insurance Marketplace, a spouse’s plan, or Medicaid.

- Myth: COBRA is Perpetual. COBRA coverage is for a limited duration, typically 18 or 36 months, though certain COBRA extensions (like for disability or second qualifying events) can extend it slightly. It is not a permanent solution.

- Myth: Missing the Election Deadline Means You Can Never Get COBRA. Generally, yes. The 60-day election period is a hard deadline. Missing it usually means forfeiting your right to COBRA coverage for that qualifying event.

- Myth: COBRA Covers All Past Medical Bills. COBRA coverage begins retroactively from the date your employer-sponsored plan ended, provided you elect and pay for it within the specified timelines. It does not cover medical bills incurred before your original plan’s end date.

- Myth: All Employers Must Offer COBRA. Only group health plans maintained by employers with 20 or more employees on more than 50% of its typical business days in the previous calendar year are generally subject to federal COBRA. Smaller employers may be subject to state-specific ‘mini-COBRA’ laws, which have different rules.

Understanding these truths about COBRA is essential for making informed decisions and avoiding costly errors, especially when planning for COBRA extensions 2026.

The Role of the Department of Labor (DOL) and IRS in COBRA

The administration and oversight of COBRA are primarily divided between two federal agencies: the Department of Labor (DOL) and the Internal Revenue Service (IRS).

The DOL, through its Employee Benefits Security Administration (EBSA), is responsible for enforcing COBRA’s disclosure and notification requirements. This means they ensure that plan administrators provide timely and accurate information to qualified beneficiaries about their COBRA rights, election periods, and coverage options. The DOL also provides guidance and assistance to workers and employers regarding COBRA compliance. If you believe your COBRA rights have been violated or you haven’t received appropriate notices, the DOL is the agency to contact.

The IRS, on the other hand, is responsible for enforcing the tax provisions related to COBRA. This includes ensuring that group health plans meet COBRA requirements to maintain their tax-favored status. The IRS also issues regulations and guidance concerning the tax implications of COBRA premiums and compliance. While beneficiaries don’t typically interact directly with the IRS regarding their COBRA rights, their regulations underpin the entire COBRA framework.

Both agencies play a critical role in ensuring that COBRA operates as intended, providing a safety net for millions of Americans. Any significant COBRA extensions 2026 or changes would likely involve guidance or regulations from both the DOL and the IRS.

Conclusion: Staying Prepared for COBRA Extensions 2026

The prospect of losing employer-sponsored health coverage can be daunting, but COBRA provides a crucial pathway to continued care. As we look towards 2026, understanding the standard COBRA rules, potential COBRA extensions, and, most importantly, the critical deadlines, is non-negotiable. While broad, government-mandated COBRA extensions 2026 akin to pandemic relief are not currently anticipated, individuals must remain vigilant for any legislative or regulatory updates that could impact their coverage options.

Proactive engagement, meticulous record-keeping, and a thorough comparison of COBRA with alternative health insurance options like the Health Insurance Marketplace are your best strategies for ensuring uninterrupted health coverage. By being informed about qualifying events, election periods, and premium payment deadlines, you empower yourself to make the best decisions for your health and financial future. Remember, your health is paramount, and understanding your COBRA rights and options for 2026 is a vital step in protecting it.