Proposed Tax Law Changes 2026: Impact on 60% of Households

The financial landscape for millions of American households is on the cusp of a significant transformation. As 2026 approaches, the specter of proposed tax law changes looms large, with projections indicating that these adjustments could directly affect a staggering 60% of households across the nation. This isn’t merely a tweak to a few lines on a tax form; it represents a potential seismic shift in personal finance, investment strategies, and overall economic stability for a substantial portion of the population. Understanding these impending changes is not just about compliance; it’s about proactive planning, strategic adaptation, and safeguarding your financial future.

The current tax framework, largely shaped by the Tax Cuts and Jobs Act (TCJA) of 2017, is set to expire or undergo significant modifications in 2026. This sunset provision was built into the legislation, meaning many of its key provisions were designed to be temporary. As that deadline approaches, lawmakers are grappling with how to proceed, leading to a flurry of proposals that could dramatically alter tax liabilities for individuals and families. The implications are far-reaching, touching everything from income tax rates and deductions to estate planning and business incentives. For many, the question isn’t if they will be affected, but how profoundly.

This comprehensive guide aims to dissect the proposed tax law changes for 2026, offering clarity on what to expect, who stands to gain or lose, and crucially, how you can begin preparing today. We’ll delve into the specifics of various proposals, analyze their economic impact, and provide actionable insights to help you navigate this complex financial terrain. Whether you’re a high-income earner, a middle-class family, or someone on a fixed income, these changes will likely touch your wallet. Being informed is the first step towards being prepared.

The Looming Sunset of TCJA Provisions: Why 2026 Matters

At the heart of the upcoming tax law changes is the expiration of several key provisions enacted under the Tax Cuts and Jobs Act (TCJA) of 2017. When the TCJA was passed, many of its individual tax provisions were set to expire at the end of 2025. This means that without new legislation, the tax code will revert to its pre-TCJA state in 2026, or at least a modified version of it. This sunset was a political compromise, allowing the bill to pass with a simple majority in the Senate by avoiding a permanent increase to the national debt projection beyond a certain threshold.

Key TCJA Provisions Set to Expire:

- Individual Income Tax Rates: The lower individual income tax rates for most brackets are scheduled to revert to higher pre-TCJA levels. This alone could mean a higher tax bill for many.

- Standard Deduction: The significantly increased standard deduction amounts are set to decrease, which could push more taxpayers back into itemizing deductions or result in a higher taxable income for those who previously took the standard deduction.

- State and Local Tax (SALT) Deduction Cap: The $10,000 cap on the SALT deduction is slated to disappear, potentially benefiting high-income earners in states with high property and income taxes. However, the overall impact depends on other deductions.

- Child Tax Credit (CTC): While the CTC was enhanced by the TCJA, some of its more generous aspects, like the increased credit amount and expanded refundability, could be scaled back.

- Personal Exemptions: The TCJA eliminated personal exemptions, but if the law reverts, personal exemptions could be reinstated, potentially reducing taxable income for larger families.

- Estate Tax Exemption: The doubled estate tax exemption amount is also set to expire, meaning more estates would be subject to federal estate taxes.

- Miscellaneous Itemized Deductions: The elimination of various miscellaneous itemized deductions (e.g., unreimbursed employee expenses) could be reversed.

The expiration of these provisions creates a legislative vacuum that Congress must address. The political climate will heavily influence what new tax law changes are ultimately passed. Will lawmakers extend some or all of the TCJA’s individual provisions? Will they propose an entirely new tax framework? The answers to these questions will determine the precise impact on households. The uncertainty surrounding these expiring provisions is a primary driver of the projected impact on 60% of households, as a return to pre-TCJA rules could mean higher taxes for many middle-income families who benefited from the increased standard deduction and lower rates.

Who Will Be Affected by the Proposed Tax Law Changes?

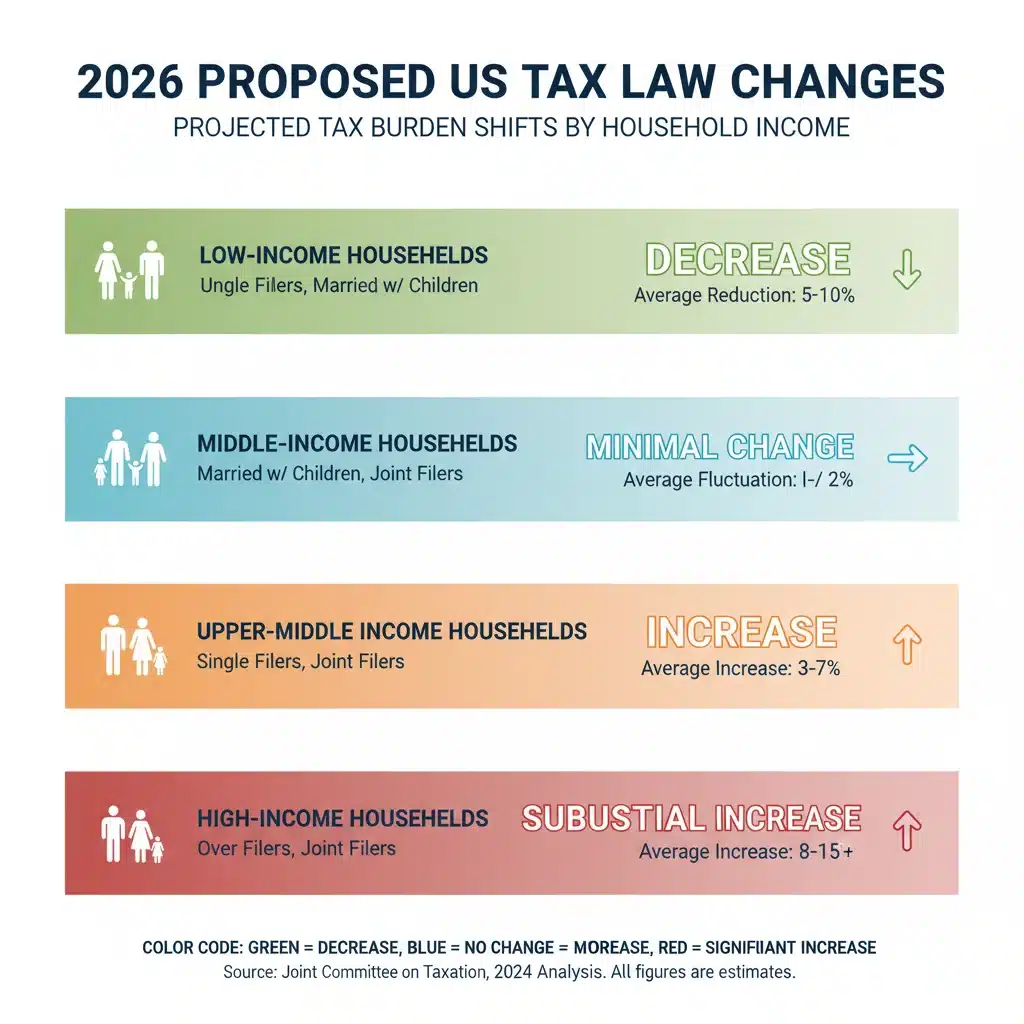

The claim that 60% of households could be affected by the proposed tax law changes in 2026 is a significant one. This broad impact stems from the widespread nature of the expiring TCJA provisions. While the exact distribution of gains and losses will depend on the final legislation, we can make informed predictions based on current proposals and the mechanics of the expiring laws.

Potential Winners and Losers:

Middle-Income Households:

Many middle-income households saw their tax bills decrease under the TCJA, primarily due to the expanded standard deduction and lower tax rates. If these provisions expire without replacement, a substantial number of these households could face higher tax liabilities. The increased standard deduction simplified tax filing for many, reducing the need to itemize. Its reduction could mean a higher taxable income for those who don’t have enough itemized deductions to surpass the new, lower threshold.

High-Income Households:

High-income earners also benefited from lower top marginal tax rates under the TCJA. If these rates revert to higher levels, their tax burden will increase. However, the potential repeal of the SALT deduction cap could offer some relief to wealthy individuals in high-tax states. The net effect for high-income households will be a complex calculation, balancing higher rates against potentially larger deductions.

Families with Children:

The TCJA significantly expanded the Child Tax Credit (CTC), making it more valuable for many families. If these enhancements are scaled back or expire, families with children could see a notable reduction in their tax benefits. This could particularly impact lower and middle-income families who rely on the CTC to offset household expenses.

Business Owners and Investors:

While the corporate tax rate reduction under the TCJA was permanent, many pass-through businesses (S-corps, partnerships, sole proprietorships) benefited from the 20% qualified business income (QBI) deduction, which is also set to expire. The loss of this deduction could increase the tax burden for many small and medium-sized business owners. Investors could also be affected by potential changes to capital gains tax rates or other investment-related deductions.

Estate Planning:

The doubled estate tax exemption provided by the TCJA allowed a significant number of wealthy individuals to pass on more assets to their heirs tax-free. If this exemption reverts to its pre-TCJA level, more estates will be subject to federal estate taxes, impacting estate planning strategies for affluent families.

It’s crucial to remember that these are general trends. The specific impact on any given household will depend on a myriad of factors, including income level, marital status, number of dependents, state of residence, and individual financial decisions. The 60% figure underscores the broad reach of these potential tax law changes, emphasizing the need for widespread awareness and preparation.

Analyzing the Economic Impact of Proposed Tax Law Changes

Beyond individual household budgets, the proposed tax law changes have significant implications for the broader economy. Tax policy is a powerful lever that can influence consumer spending, business investment, and overall economic growth. Understanding these larger ripple effects is essential for comprehending the full scope of the 2026 tax landscape.

Impact on Consumer Spending:

If a large number of middle-income households face higher tax bills due to expiring provisions, it could lead to a reduction in disposable income. This, in turn, could dampen consumer spending, which is a major driver of economic activity. Less spending on goods and services could slow economic growth, affect retail sectors, and potentially lead to job losses in consumer-facing industries. Conversely, if certain tax breaks are extended or new ones introduced that favor lower and middle-income groups, it could stimulate spending.

Business Investment and Job Creation:

The expiration of the qualified business income (QBI) deduction could increase the tax burden on pass-through businesses, which represent a significant portion of the American economy. Higher taxes for these businesses might reduce their capacity for investment in expansion, research and development, or hiring new employees. This could slow job creation and curb innovation. On the other hand, if new tax incentives for specific industries or green technologies are introduced, they could spur investment in those areas.

National Debt and Government Revenue:

The decisions made regarding the expiring TCJA provisions will have a direct impact on government revenue and the national debt. Extending the lower tax rates and higher deductions could lead to a larger national debt, while allowing them to expire would likely increase government revenue. This fiscal consideration will be a central point of debate among policymakers, balancing the need for revenue against the desire to stimulate economic growth and provide tax relief to citizens. Any new tax law changes will be scrutinized for their long-term fiscal sustainability.

Inflationary Pressures:

Tax policy can also play a role in inflationary pressures. If tax cuts are enacted that significantly boost consumer demand without a corresponding increase in supply, it could exacerbate inflation. Conversely, tax increases that reduce disposable income could help cool an overheating economy. The timing and nature of the 2026 tax law changes will be critical in the ongoing battle against inflation.

Wealth Inequality:

Changes to the estate tax exemption and capital gains taxes could further impact wealth inequality. A lower estate tax exemption, for instance, could lead to more wealth redistribution over generations, while higher capital gains taxes could affect the accumulation of wealth through investments. The political debate around these changes often centers on their perceived fairness and impact on different socioeconomic groups.

The economic impact of the 2026 tax law changes is multifaceted and complex. It’s not just about individual tax bills but about the health and direction of the entire economy. Policymakers will be navigating a delicate balance, trying to address fiscal concerns while promoting economic stability and growth. For households, understanding this broader context can help in anticipating how these changes might indirectly affect their employment, investments, and overall financial well-being.

Strategies for Proactive Financial Planning Amidst Uncertainty

Given the significant potential for tax law changes in 2026, proactive financial planning is not just advisable; it’s essential. Waiting until new legislation is finalized could leave you scrambling to adapt. By taking steps now, you can position yourself to mitigate negative impacts and potentially capitalize on new opportunities. Here are some key strategies:

1. Review Your Current Tax Situation:

Start by understanding how the current tax laws affect you. Look at your past tax returns to identify which TCJA provisions have benefited you the most (e.g., standard deduction vs. itemizing, child tax credit, QBI deduction). This will give you a baseline to assess the potential impact of changes. Consider running hypothetical scenarios under pre-TCJA rules to get a rough idea of how your tax liability might shift.

2. Maximize Tax-Advantaged Accounts:

Regardless of future tax law changes, contributing to tax-advantaged retirement accounts like 401(k)s, IRAs (Traditional or Roth), and HSAs remains a sound strategy. These accounts offer tax benefits now (deductions for contributions) or in retirement (tax-free withdrawals), providing a hedge against future tax rate fluctuations. If you anticipate higher tax rates in the future, contributing to a Roth IRA or Roth 401(k) might be particularly appealing, as you pay taxes now on contributions and withdraw tax-free later.

3. Consider Tax Loss Harvesting:

If you have investments, consider tax loss harvesting before the end of 2025. This involves selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income. If capital gains rates increase in 2026, having harvested losses could be even more valuable. Consult with a financial advisor to determine if this strategy is appropriate for your portfolio.

4. Re-evaluate Your Estate Plan:

With the estate tax exemption potentially reverting to lower levels, now is an opportune time to review and update your estate plan. Consider strategies like gifting, establishing trusts, or other wealth transfer techniques that could help reduce potential estate tax liability under future rules. This is particularly relevant for affluent individuals and families.

5. Optimize Business Deductions and Structures:

For business owners, understanding the potential expiration of the QBI deduction is critical. Work with your tax advisor to explore alternative business structures or strategies that could help minimize your tax burden if the QBI deduction is not extended. This might involve re-evaluating your legal entity structure or timing of income and expenses.

6. Stay Informed and Seek Professional Advice:

The legislative process is dynamic, and the final tax law changes for 2026 are still uncertain. Stay informed by following reputable financial news sources and official government updates. Most importantly, consult with a qualified financial advisor or tax professional. They can provide personalized advice based on your specific financial situation, help you understand the proposed changes, and guide you in developing an effective strategy.

The Political Landscape and Future Tax Legislation

The ultimate form of the 2026 tax law changes will be heavily influenced by the political landscape. With a presidential election in 2024 and ongoing shifts in congressional control, the debate over tax policy is likely to be intense and partisan. Different political parties often have vastly different philosophies on taxation, particularly regarding income distribution, corporate taxes, and the role of government in the economy.

Key Political Considerations:

- Partisan Divisions: The current political climate is highly polarized. Democrats often advocate for higher taxes on corporations and high-income earners to fund social programs and reduce wealth inequality, while Republicans typically favor lower taxes across the board to stimulate economic growth. This fundamental disagreement makes bipartisan compromise challenging.

- Election Outcomes: The results of the 2024 presidential and congressional elections will significantly shape the direction of tax policy. A change in presidential administration or control of Congress could lead to a dramatically different approach to the expiring TCJA provisions.

- Economic Conditions: The state of the economy in late 2025 and 2026 will also play a crucial role. If the economy is struggling, policymakers might lean towards tax cuts to stimulate growth. If inflation remains a concern, tax increases or targeted fiscal policies might be considered.

- Public Opinion: Public sentiment regarding tax fairness and economic burden will undoubtedly influence lawmakers. Advocacy groups and public discourse will shape the narrative around who should bear the brunt of tax changes and who should receive relief.

- Budgetary Constraints: The national debt and ongoing budget deficits will be a constant backdrop to any tax reform discussions. Lawmakers will need to consider the revenue implications of their decisions, potentially leading to difficult trade-offs.

Given this complex political environment, it’s highly unlikely that Congress will simply allow all TCJA provisions to expire without any action. A more probable scenario involves a combination of extensions, modifications, and potentially new tax policies. Some provisions might be made permanent, others might be extended for a shorter period, and new credits or deductions could be introduced to address current economic or social priorities. The final package of tax law changes will be the result of intense negotiation and compromise.

For individuals and businesses, this political uncertainty underscores the importance of flexible financial planning. Rather than betting on a specific outcome, it’s prudent to develop strategies that can adapt to various scenarios. Diversifying investments, maintaining emergency savings, and having a clear understanding of your financial goals will be paramount in navigating this period of flux.

Understanding the Nuances: Beyond Income Tax Rates

While much of the discussion around tax law changes often centers on income tax rates, it’s essential to remember that the tax code is far more intricate. Several other areas could see significant alterations in 2026, each with its own specific impact on households.

Capital Gains and Dividends:

The tax rates on long-term capital gains and qualified dividends were also adjusted under the TCJA. While these rates were not explicitly set to expire in the same way as individual income tax rates, they are often linked to ordinary income tax brackets. If ordinary income tax rates revert to higher levels, it’s possible that capital gains and dividend rates could also see adjustments, particularly for high-income earners. This would directly affect investors and retirees relying on investment income.

Alternative Minimum Tax (AMT):

The TCJA significantly curtailed the reach of the Alternative Minimum Tax (AMT) by increasing exemption amounts and phase-out thresholds. If these reverts, more taxpayers, particularly upper-middle-income individuals and those with certain deductions, could find themselves subject to the AMT again. The AMT is a parallel tax system designed to ensure that wealthy individuals pay at least a minimum amount of tax, regardless of deductions. Its re-expansion could complicate tax planning for many.

Itemized Deductions and Credits:

Beyond the SALT cap, other itemized deductions that were eliminated or limited by the TCJA could be reinstated or altered. For example, some miscellaneous itemized deductions (like unreimbursed employee expenses) might return. Similarly, various tax credits, beyond the Child Tax Credit, could be subject to review and modification. These smaller, often overlooked changes can still have a cumulative effect on a household’s overall tax liability.

Business Tax Provisions for Individuals:

While the corporate tax rate was permanently lowered, many individual business owners, freelancers, and gig economy workers benefited from the Qualified Business Income (QBI) deduction. The expiration of this deduction could significantly increase the tax burden for these individuals. Lawmakers might consider alternative ways to incentivize small business growth if the QBI deduction is allowed to expire.

International Tax Considerations:

For individuals with international income or assets, changes to foreign tax credit rules, expatriation taxes, or other international provisions could also be on the table. While these affect a smaller percentage of the population, their impact can be substantial for those concerned. The global tax landscape is always evolving, and U.S. tax policy often reacts to these changes.

The complexity of the tax code means that the proposed tax law changes will have ripple effects across many different provisions. A holistic view is necessary to fully grasp their impact. This is another reason why professional guidance is invaluable, as tax professionals are equipped to analyze these intricate connections and provide comprehensive advice.

Conclusion: Preparing for the Financial Future

The projected impact of proposed tax law changes on 60% of households in 2026 underscores one undeniable truth: the financial future is rarely static. The expiration of key TCJA provisions creates an environment of significant uncertainty and potential transformation for millions of Americans. From shifts in individual income tax rates and the standard deduction to changes in the Child Tax Credit and estate tax exemptions, the breadth of these potential alterations demands attention and strategic foresight.

While the precise details of the 2026 tax code remain subject to political negotiation and evolving economic conditions, the time to prepare is now. Proactive financial planning involves understanding your current tax situation, exploring tax-advantaged savings vehicles, optimizing investment strategies, and reviewing your estate plan. It’s about building resilience into your financial framework so that you can adapt to whatever legislative outcomes emerge.

The journey through these impending tax law changes doesn’t have to be navigated alone. Engaging with qualified financial advisors and tax professionals can provide invaluable guidance, helping you to interpret complex legislation, anticipate potential impacts, and craft a personalized strategy that aligns with your financial goals. Their expertise can transform uncertainty into opportunity, ensuring that you are well-positioned to thrive in the evolving economic landscape.

Ultimately, the message is clear: 2026 is not just another year on the calendar. It represents a pivotal moment for personal finance in America. By staying informed, planning strategically, and seeking expert advice, households can empower themselves to navigate the forthcoming tax law changes with confidence and secure a more stable financial future.